The Truth about the Abenomics Growth Streak

SNA (Tokyo) — The Abe government and sections of the business community are celebrating an unusually long seven quarters of sustained economic growth in Japan. This is sometimes portrayed as evidence that Abenomics is finally coming into its own and as proof that the Liberal Democratic Party is particularly adept at economic management.

Indeed, out on the campaign trail, some ruling party politicians have argued that voters should stick with them, lest the opposition parties regain control and thrust the nation back into the dark days of economic mismanagement seen in the Democratic Party of Japan era.

This political attack remains potent mainly because the big business community and the news media fail to explain the broader economic facts.

As has been widely advertised, the main objective of the Abenomics program is to spur growth in the Japanese economy and to make the nation strong once again. For that purpose, massive amounts of money have been pumped into the economy to lower the value of the yen (thus making the prices of Japanese exports more competitive internationally) and to stimulate the domestic economy with increased inflation and spending.

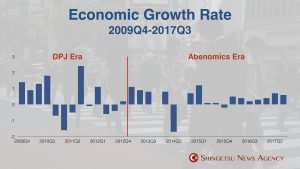

One point that the Abe government never mentions can be seen in this chart:

A dirty secret is that national economic growth rates were actually higher under the supposedly incompetent Democratic Party of Japan government—notwithstanding the March 11 tsunami and the Fukushima Daiichi disaster—than they have been during the Abe government’s period of massive spending.

To wit, the annualized growth rate under the Hatoyama, Kan, and Noda administrations was about 1.6%; the annualized growth rate under Abenomics has been just under 1.5%.

Where Abenomics has indeed shined is in terms of inflating the stock market. During the 2009-2012 Democratic Party of Japan period, the stock market was stagnant, but in the Shinzo Abe period it has boomed, more than doubling its value since 2013.

In other words, Abenomics’ good reputation in the media may derive largely from the fact that businesses and investors in the stock market have done very well under its regime, even while economic growth for the benefit of the Japanese public as a whole hasn’t been particularly outstanding.

Takuji Okubo, managing director and chief economist at Japan Macro Advisors, offers the following evaluation: “The Japanese economy has been doing better since Abe became the prime minister at the end of 2012. I would attribute 30% of it to Prime Minister Abe’s insistence that the Bank of Japan adopted the 2% inflation target and 70% to external factors, chiefly the steady upturn in the global economy in the past five years.”

Martin Schulz, senior research fellow at Fujitsu Research Institute, points to the “missing arrow” of Abenomics as a concern going forward: “Productivity, the long-term driver of growth, is not going up, which is due to the lack of ‘structural’ reforms under Abenomics. Only if this changes could the potential growth rate go to where the actual growth rate of just above 1% (artificially by monetary stimulus) has been during Abenomics.

The implication is that while Prime Minister Shinzo Abe’s policy of massively ramping up stimulus spending may make the Japanese economy seem like it is going quite well under his regime, his preference for engagement in rightwing political projects, such as stomping down non-existent conspiracies or revising the Constitution, has diverted government attention from carrying out the crucial economic reforms that might boost performance into the 2020s, and thus justify the manner in which Abenomics continues to pile up Japan’s public debt.

For breaking news, follow on Twitter @ShingetsuNews